|

|

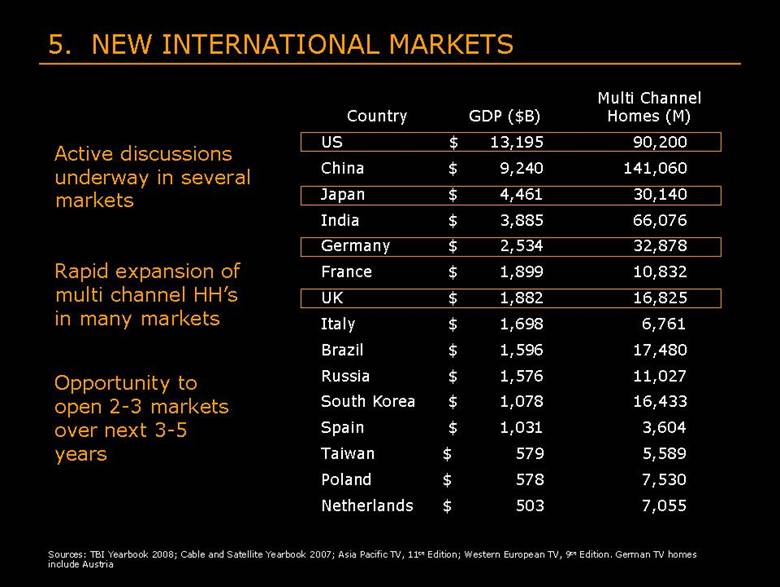

5. NEW

INTERNATIONAL MARKETS Active discussions underway in several markets Rapid

expansion of multi channel HH’s in many markets Opportunity to open 2-3

markets over next 3-5 years 7,055 $ 503 Netherlands 7,530 $ 578 Poland 5,589 $ 579 Taiwan 3,604 $ 1,031 Spain 16,433 $ 1,078 South Korea 11,027 $ 1,576 Russia

17,480 $ 1,596 Brazil 6,761 $ 1,698 Italy 16,825 $ 1,882 UK 10,832 $ 1,899 France

32,878 $ 2,534 Germany 66,076 $ 3,885 India 30,140 $ 4,461 Japan 141,060 $ 9,240

China 90,200 $ 13,195 US Multi Channel Homes (M) GDP ($B) Country Sources:

TBI Yearbook 2008; Cable and Satellite Yearbook 2007; Asia Pacific TV, 11th

Edition; Western European TV, 9th Edition. German TV homes include Austria

|